One breach is all it takes to end a small business. That is not fear-mongering. It is math. A single data breach now costs businesses nearly $3 million on average once you add fines, legal fees, and lost customers. Add in non-compliance penalties from your bank, and the number climbs even higher. Yet many small business owners still treat their PCI compliance checklist like a once-a-year chore they rush through before an audit.

That approach no longer works. PCI DSS 4.0.1 is now the only active version of the standard, and every “future-dated” requirement that used to be optional is mandatory. Assessors expect proof that your security controls run all year, not just on the day of the scan. This guide breaks down exactly what belongs on your PCI compliance checklist for 2026, why it matters, and how to build a program you can actually sustain without a dedicated IT department.

What Is PCI Compliance and Why It Matters for Small Businesses

PCI compliance means following the Payment Card Industry Data Security Standard, a set of rules created to protect cardholder data. It applies to any business that accepts, stores, processes, or transmits credit or debit card information. Store size does not matter. A single-location coffee shop and a national retail chain both fall under the same standard, though the validation path differs.

PCI DSS is not a government law. It is a contractual requirement enforced by the major card brands, including Visa, Mastercard, American Express, Discover, and JCB. You can review the official standard directly on the PCI Security Standards Council website. Your acquiring bank and payment processor require compliance as a condition of letting you accept card payments at all. Skip it, and you risk monthly fines, higher processing rates, and in serious cases, the loss of your ability to take card payments entirely.

For small businesses, the stakes are personal. Most small merchants cannot absorb a $50,000 non-compliance fine or the reputational damage of a public breach announcement. A strong PCI compliance checklist protects your revenue, your customer relationships, and your ability to keep operating.

PCI DSS 4.0.1: What Changed and Why 2026 Is Different

PCI Security Standards Council (PCI SSC)

The PCI Security Standards Council (PCI SSC) is the global body that writes and maintains the PCI DSS framework. It is made up of the major card brands and works with security assessors, banks, and merchants to update the standard as threats evolve. The council retired PCI DSS 3.2.1 at the end of 2024, making version 4.0.1 the only valid version going into 2026.

Version 4.0.1, published in June 2024, is a minor correction to version 4.0. It did not add new requirements or shift deadlines. What it did was clean up language and close gray areas that businesses had been struggling to interpret. The bigger story is the deadline behind it: the transition period for PCI DSS 4.0 officially ended on March 31, 2025. Every requirement that was once labeled “best practice” or “future-dated” is now a hard requirement your assessor will check.

The philosophy shift matters more than any single technical control. PCI DSS 4.0.1 moves the entire industry away from a once-a-year audit snapshot and toward continuous, year-round compliance. Assessors now expect documented evidence that your firewalls, access controls, and monitoring tools worked every day of the year, not just during your scheduled assessment window. If your current approach is a mad scramble every twelve months, 2026 is the year to fix that.

The standard also formalized something called the Customized Approach. Instead of forcing every business into the same rigid technical box, this path lets you meet a security objective using a different control that fits your specific technology stack, as long as you can document and justify it. This flexibility helps small businesses running modern, cloud-based point-of-sale systems that do not always match the traditional on-premise model the standard was originally written for.

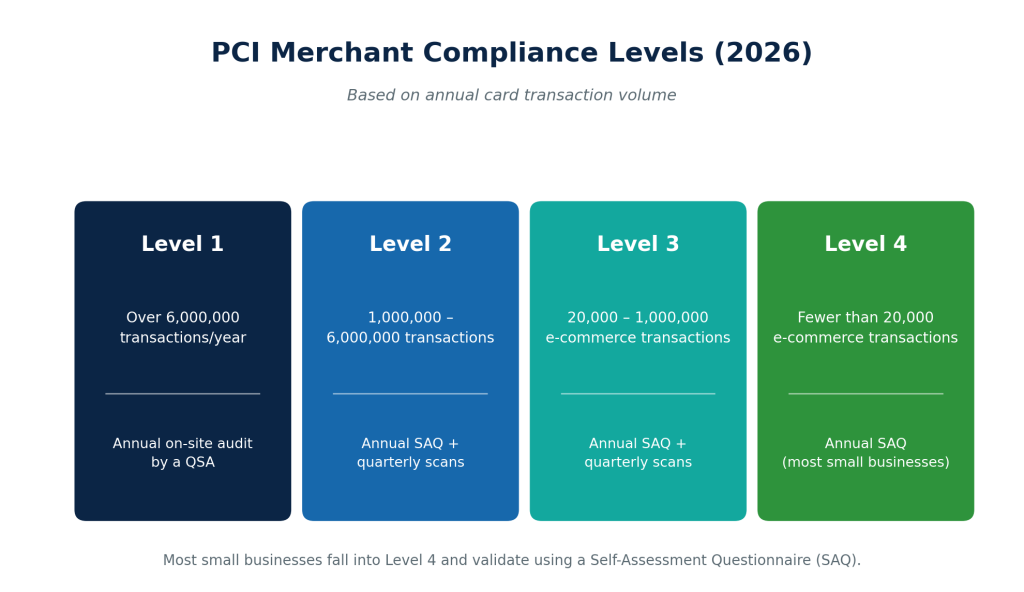

Determine Your PCI Compliance Level First

Before you can build an accurate PCI compliance checklist, you need to know which merchant level applies to your business. The PCI SSC and card brands sort merchants into four levels based on annual transaction volume, and your level decides how you validate compliance.

- Level 1 merchants process more than six million card transactions a year across all channels and must complete an annual on-site audit performed by a Qualified Security Assessor, along with a formal Report on Compliance.

- Level 2 merchants handle between one million and six million transactions annually and typically validate through a Self-Assessment Questionnaire plus quarterly vulnerability scans, though some card brands still require an assessor review.

- Level 3 merchants process between 20,000 and one million e-commerce transactions a year and follow a similar SAQ-plus-scanning path. Level 4 merchants, which cover the vast majority of small businesses, process fewer than 20,000 e-commerce transactions or under one million total transactions annually. Most

- Level 4 businesses can self-validate through a Self-Assessment Questionnaire without hiring an outside assessor, which keeps costs manageable.

Figure 1: PCI merchant compliance levels are based on annual card transaction volume.

Knowing your level early saves time. It tells you exactly which Self-Assessment Questionnaire type applies to your business and which of the twelve PCI DSS requirements you actually need to document.

The Complete PCI Compliance Checklist: 12 Requirements Explained

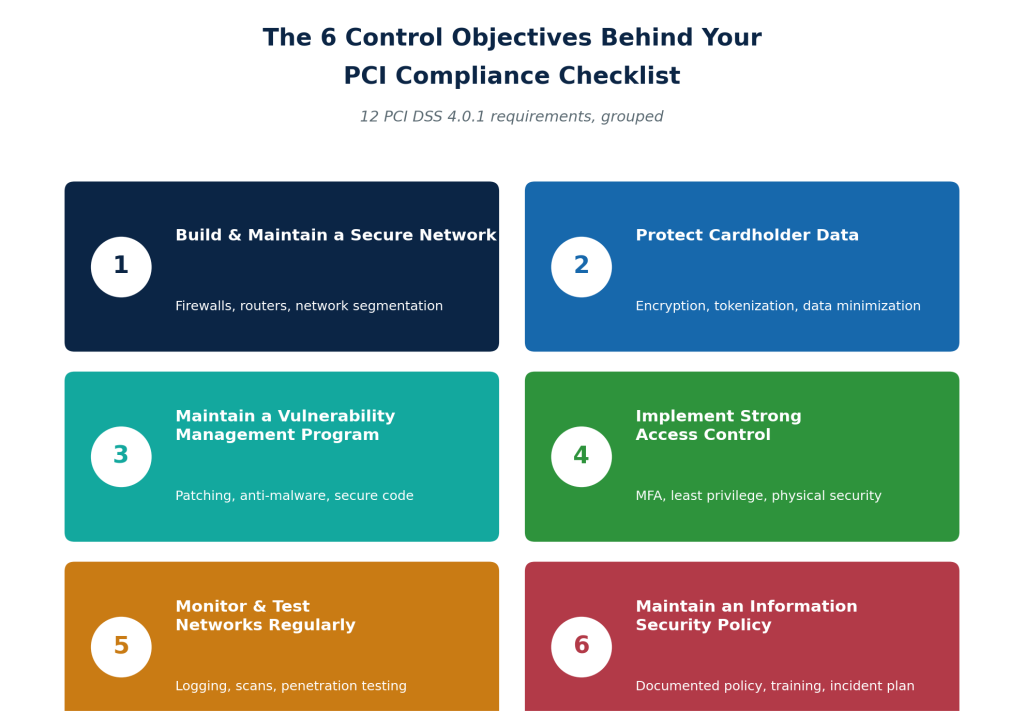

The PCI DSS framework organizes its requirements into six broader control objectives. These groupings have stayed remarkably stable since the standard was first introduced, even through the jump from version 3.2.1 to 4.0.1. Understanding them in context makes your PCI compliance checklist far easier to follow than treating each requirement as an isolated rule.

Figure 2: The 12 PCI DSS requirements roll up into six control objectives.

Build and Maintain a Secure Network and Systems

Your first line of defense is a properly configured firewall and router setup that separates your cardholder data environment from the rest of your network and from the public internet. This includes segmenting your point-of-sale systems from your general office Wi-Fi, disabling default vendor passwords and settings on every device, and documenting your network diagram so you and any assessor can see exactly where card data travels. Small businesses running consumer-grade routers straight out of the box are one of the most common audit failures in this category.

Protect Cardholder Data

This objective covers how you store, transmit, and dispose of card data. Under PCI DSS 4.0.1, full disk encryption alone is no longer accepted as a way to protect stored cardholder data at rest, since it only protects data while a device is powered off. Businesses need field-level or database-level encryption instead. The safest strategy for most small merchants is simply not storing card numbers at all. Tokenization and point-to-point encryption, offered by most modern payment processors, replace the actual card number with a meaningless token, which shrinks your compliance scope dramatically. You should also confirm you are encrypting cardholder data during transmission across open, public networks using strong, current cryptographic protocols.

Maintain a Vulnerability Management Program

This requirement group covers keeping your systems patched, running anti-malware protection, and writing secure code if you maintain your own website or checkout process. PCI DSS 4.0.1 requires that critical security patches be installed within 30 days of release. You also need a documented process for identifying and ranking vulnerabilities so the most dangerous ones get fixed first, rather than working through patches in whatever order they arrive.

Implement Strong Access Control Measures

Access control is about limiting who can see cardholder data and verifying they are who they claim to be. Every employee and administrator with any access to your cardholder data environment now needs multi-factor authentication, combining something they know, like a password, with something they have or something they are, such as a hardware token or biometric scan.

Passwords alone are no longer considered sufficient under the current standard; CISA’s guidance on multi-factor authentication is a useful starting point for setting this up correctly. You should also enforce the principle of least privilege, meaning employees only get access to the systems and data they genuinely need for their job, and you should review those permissions on a regular schedule. Physical security matters here too: point-of-sale terminals, server rooms, and any hardware handling card data need to be physically secured against tampering or theft.

Monitor and Test Networks Regularly

Continuous monitoring is the heart of the 4.0.1 philosophy shift. You need logging systems that track access to cardholder data and alert your team to suspicious activity, quarterly external vulnerability scans performed by an Approved Scanning Vendor, and periodic penetration testing to find weaknesses before an attacker does. If you run an e-commerce checkout page, this is also where the newer script-monitoring requirements live.

Requirement 6.4.3 requires you to maintain a documented inventory of every script running on your payment page, confirm who authorized it, and verify its integrity. Requirement 11.6.1 requires a change- and tamper-detection mechanism that checks your payment page for unauthorized changes at least weekly. Both requirements exist because of a rise in e-skimming attacks, sometimes called Magecart-style attacks, where criminals inject malicious code into checkout pages to silently steal card numbers as customers type them in.

Maintain an Information Security Policy

The final objective ties everything together in writing. You need a documented, formal information security policy that covers acceptable use of technology, incident response procedures, employee security training, and vendor management for any third party that touches your cardholder data. This is also where your scoping documentation lives. Requirement 12.5.2 requires you to formally document your cardholder data environment and confirm your scoping process, ideally reviewed alongside a Qualified Security Assessor even if your business only requires self-assessment.

Choosing the Right Self-Assessment Questionnaire

Not every business fills out the same paperwork. The Self-Assessment Questionnaire, or SAQ, comes in several versions, and picking the right one depends on how you accept payments. Getting this classification wrong is one of the most expensive mistakes a small business can make, because it either leaves real gaps in your security or forces you to complete far more paperwork than necessary. When in doubt, your acquiring bank or a Qualified Security Assessor can confirm which SAQ actually applies to your setup.

| SAQ Type | Who It’s For | Key Obligation |

| SAQ A | Fully outsourced payment processing, no card data stored electronically | Simplest questionnaire; confirm outsourcing and basic controls |

| SAQ A-EP | E-commerce merchants embedding a third-party payment form on their own page | Payment page script inventory and weekly tamper checks |

| SAQ D | Merchants who process, store, or transmit card data directly | Full scope of applicable PCI DSS 4.0.1 requirements |

What a Modern Checkout Stack Looks Like

Stripe

Stripe is one of the payment processors many small e-commerce businesses use specifically because it absorbs most of the PCI compliance burden. By hosting the actual card entry fields and handling tokenization on its own PCI-validated infrastructure, Stripe lets merchants qualify for the simpler SAQ A path, provided the merchant does not touch raw card data anywhere in their own systems. Full details on its approach to compliance are available on the Stripe PCI compliance guide.

Square

Square serves a similar role for brick-and-mortar small businesses. Its point-of-sale hardware handles card data through end-to-end encryption before it ever reaches the merchant’s own network, which significantly reduces the in-store scope a small retailer needs to secure.

Choosing a processor that handles encryption and tokenization for you is one of the single most effective moves on any PCI compliance checklist, because it shrinks the size of your cardholder data environment and, with it, the number of requirements that actually apply to your business.

How to Reduce Your PCI Compliance Scope

Scope reduction is the smartest strategy available to small businesses with limited security budgets. The less cardholder data your systems touch, store, or transmit, the fewer PCI DSS requirements apply to you. Tokenization replaces sensitive card numbers with a random, meaningless value that is useless to attackers if stolen, while point-to-point encryption scrambles card data the instant it is swiped, tapped, or entered, so it is never exposed in plain text on your network.

Outsourcing your payment page entirely to a PCI-validated processor, rather than building your own checkout form, keeps card data off your servers altogether. Segmenting your network so that point-of-sale systems sit on a separate, isolated network from your general business Wi-Fi and email systems also shrinks your cardholder data environment, since anything outside that segment falls outside your compliance scope.

The Real Cost of PCI Compliance for Small Businesses

Compliance costs vary widely depending on your transaction volume and existing security setup, but most small businesses can expect to spend somewhere between $800 and $20,000 annually. Level 4 merchants using SAQ A with an outsourced payment processor sit at the low end of that range, since they mainly pay for quarterly scans and staff time to complete the questionnaire. Businesses running their own e-commerce checkout, or those needing an outside consultant to help interpret the newer script-monitoring requirements, land at the higher end.

Compare that modest investment to the alternative: acquiring banks can levy non-compliance fines ranging from $5,000 to $100,000 per month depending on business size and how long the violation continues, and that is before counting the average multi-million-dollar cost of an actual breach.

Common Mistakes Small Businesses Make

The most frequent failure is treating PCI compliance as a once-a-year event instead of a continuous practice, which leaves real gaps for the other eleven months of the year that an assessor can no longer overlook under 4.0.1. Close behind that is misjudging SAQ eligibility, either by assuming outsourcing removes all obligations or by completing the wrong questionnaire entirely.

Many small e-commerce merchants also overlook the newer payment-page script requirements, not realizing that even a fully outsourced payment form can pull in third-party scripts that now need to be inventoried and monitored. Storing more cardholder data than necessary, often in old spreadsheets, email archives, or backup systems nobody remembers to check, is another recurring problem that dramatically expands a business’s compliance scope for no operational benefit.

Finally, many owners skip employee security training entirely, even though phishing and social engineering remain some of the most common ways attackers gain access to a small business’s systems in the first place.

Penalties for Non-Compliance You Cannot Ignore

The financial consequences of ignoring your PCI compliance checklist are steep and layered. Acquiring banks can charge monthly non-compliance fees ranging from around $5,000 to $100,000, scaled to your business size and the duration of the gap. If a breach actually occurs, the average total cost climbs into the millions once you add forensic investigation, legal fees, customer notification, credit monitoring services, and regulatory fines. Beyond the direct dollar figures, card brands can revoke your ability to process payments entirely, which for most modern small businesses is functionally equivalent to closing the doors. Reputational damage compounds all of it: customers who learn their card data was compromised rarely come back, and news of a breach travels fast in tight-knit local markets.

Conclusion

PCI compliance is not a certification you earn once and forget. It is an ongoing security discipline, and 2026 is the year that discipline becomes non-negotiable. Every requirement that used to carry a grace period is now fully enforced, and assessors expect proof that your controls ran continuously, not just on scan day. The good news is that the path forward is well defined. Identify your merchant level, choose the right Self-Assessment Questionnaire, work through the six control objectives behind the twelve PCI DSS requirements, and lean on scope-reducing tools like tokenization and outsourced payment processing wherever you can. Treat your PCI compliance checklist as a living part of how you run your business, and you protect not just your compliance status, but your customers, your reputation, and your bottom line.

Frequently Asked Questions

Is PCI compliance legally required for small businesses?

PCI DSS is not a government law, but it is effectively mandatory. Card brands and acquiring banks require it contractually as a condition of accepting Visa, Mastercard, American Express, Discover, or JCB payments. Non-compliance can trigger monthly fines and, eventually, loss of card processing privileges.

How much does PCI compliance cost a small business?

Most small businesses spend between $800 and $20,000 a year, depending on transaction volume, merchant level, and whether they outsource payment processing. Businesses using a fully outsourced processor and SAQ A generally land at the lower end of that range.

What is the difference between PCI DSS 4.0 and 4.0.1?

PCI DSS 4.0.1, released in June 2024, is a minor correction to version 4.0. It clarified wording and fixed inconsistencies but did not add new requirements or change any deadlines. Version 4.0.1 is now the only active version of the standard.

Do I still need to worry about PCI compliance if I use a third-party payment processor?

Yes. Outsourcing reduces your scope but does not eliminate it. Even merchants using SAQ A still have documented obligations, and if your own web page embeds a third-party payment form, newer script-monitoring requirements can still apply to you.

How often do I need to complete a PCI compliance checklist review?

PCI DSS 4.0.1 expects continuous compliance, not an annual snapshot. While your formal Self-Assessment Questionnaire or audit is typically completed once a year, quarterly vulnerability scans, ongoing monitoring, and regular access reviews should run all year long.