Picture this. You walk into your favorite coffee shop, glance at your phone, and a soft chime confirms your latte is paid for. No card. No cash. No fumbling for change. That moment, repeated billions of times a day, is the quiet revolution behind the rise of digital wallets. What started as a niche feature on a single iPhone model in 2014 has become the default way the planet pays.

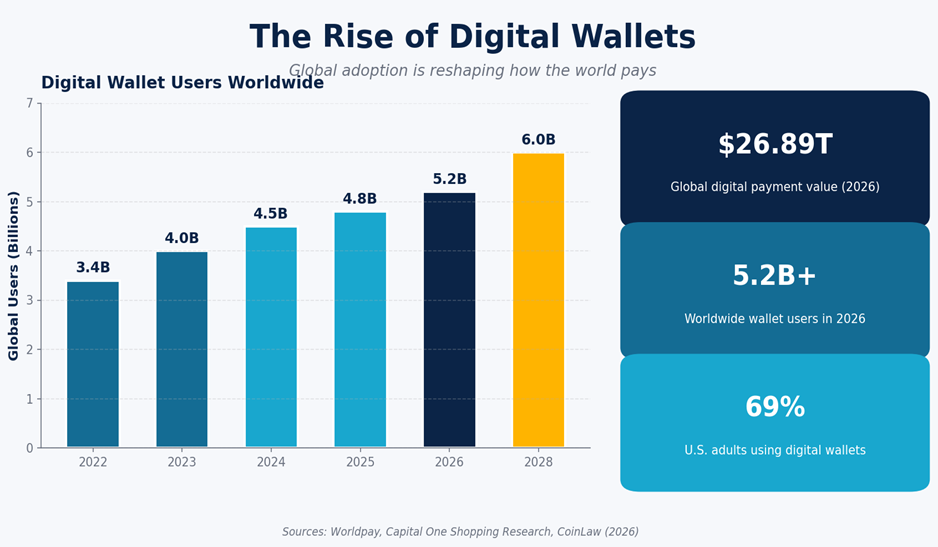

Global digital wallet adoption is on track to reach 6 billion users by 2028.

Today, more than 5.2 billion people use a digital wallet. That is over 60% of the world’s population. The combined transaction volume is projected to top $26 trillion in 2026 alone. Two names dominate the conversation in most Western markets: Apple Pay and Google Pay. But the story is bigger than any single brand. It is about contactless payments, biometric security, embedded finance, and the slow death of the physical wallet.

This guide breaks down where digital wallets stand right now, how the two biggest players actually compare, and what is coming next as stablecoins, wearables, and AI agents reshape the payment stack.

Table of Contents

What Is a Digital Wallet, Really?

A digital wallet is a software-based system that securely stores your payment credentials, identification, and increasingly, your loyalty cards, transit passes, event tickets, and even car keys. It lives on your phone, your watch, or a browser. When you tap to pay, the wallet uses Near Field Communication (NFC) or QR codes to send a tokenized version of your card details to the merchant. The actual card number never leaves your device.

That tokenization is the security trick that enabled mass adoption. Combined with biometric checks like Face ID and fingerprint scans, modern mobile wallets are arguably safer than the plastic card sitting in your back pocket. Lost your phone? The data is locked behind biometrics and can be remotely wiped. Lose your wallet, and a thief gets to swipe until you cancel.

This security-plus-convenience combo is why contactless payments have become second nature. Tap-to-pay now accounts for over 75% of in-person transactions on the Mastercard network globally.

The Numbers Behind the Mobile Payment Boom

The pace of change in the digital payments market is hard to overstate. To ground the story, here is a snapshot of the global landscape heading into 2026, with projections through the end of the decade.

| Metric | 2024 | 2026 | 2030 Projection |

| Global digital wallet users | 4.5 billion | 5.2 billion | ~6 billion |

| Annual digital payment value | $24.07 trillion | $26.89 trillion | Growing at 11.7% YoY |

| Global market valuation | ~$45 billion | $68 billion | $145 billion |

| U.S. adults using digital wallets | 62% | 69% | Expected to exceed 80% |

| POS share held by digital wallets | 30% | 32–35% | 45%+ |

Table 1: Global digital wallet adoption metrics (Sources: Worldpay, CoinLaw, SQ Magazine).

A few things jump out from that table. The user base is still growing, but the more striking shift is the value flowing through these systems. The market more than doubles between 2026 and 2030. And in the United States, the country that famously lagged Asia on contactless adoption, more than two-thirds of adults now reach for a phone or watch instead of plastic in any given month.

Asia-Pacific remains the heartland of mobile wallet usage. India leads the world with roughly 91% of consumers using digital wallets, followed closely by Indonesia and Thailand. China remains in a category of its own, with Alipay and WeChat Pay together handling more than 90% of the country’s mobile wallet transactions. To dig deeper into the macro shift, the World Economic Forum has a strong overview of how digital assets are reshaping global finance, available at

Apple Pay

How Apple Pay Built the Premium Playbook

Apple launched Apple Pay in October 2014 alongside the iPhone 6, and for years it defined what a mainstream digital wallet should feel like. The pitch was simple. Hold your phone near a contactless terminal, authenticate with Touch ID, and you are done. The actual card number is replaced by a device-specific token, and Apple does not see the transaction details.

That security-first design, paired with a tightly controlled hardware ecosystem, gave Apple Pay an unfair advantage in the United States. As of 2026, Apple Pay holds roughly 57% of the U.S. mobile wallet market. The service is live in 95 countries and supported by more than 11,000 banks. Estimated global users sit around 744 million, and the platform is projected to process about $8.7 trillion in transactions during 2026.

Apple’s strategy has always been ecosystem lock-in. Apple Pay only works on Apple devices. Apple Wallet now stores your credit cards, transit cards, hotel keys, driver’s licenses in select U.S. states, and even your COVID vaccination history. The Apple Card, launched in 2019, deepens the moat. So does Apple Pay Later, the company’s push into buy-now-pay-later, which is on track to handle over $1.2 billion in microloans by the end of 2026. The trade-off, of course, is that none of this works if you switch to Android.

Google Pay

How Google Pay Plays the Open-Ecosystem Card

Google launched its first wallet product in 2015 and rebranded it as Google Pay, then merged the payments and pass-storage features into Google Wallet across most regions. The strategy is the mirror image of Apple’s. Where Apple optimizes for one premium ecosystem, Google chases scale across every Android device on the planet.

That bet is paying off. Google Pay and Google Wallet together serve an estimated 820 million active users globally, more than Apple, even though the U.S. revenue per user is lower. Google Wallet is live in 86 countries and is the dominant mobile wallet in India, Southeast Asia, and large parts of Africa, where Android dominates the smartphone market. In 2026, Google Pay is projected to process around $5.2 trillion in global transactions.

Google’s open philosophy shows up in the product details. Google Wallet integrates with hundreds of transit systems, supports digital IDs in supported regions, and works across Wear OS smartwatches without lock-in to a single hardware brand. The company is also piloting savings accounts and deeper financial services for Gen Z users, betting that the next billion wallet users will treat the app as their primary banking interface, not just a tap-to-pay tool.

Figure 2: A side-by-side look at how Apple Pay and Google Pay stack up in 2026.

Apple Pay vs. Google Pay: A Direct Comparison

Both services do the same core job, which is to let you tap your phone to pay. The differences show up in scope, ecosystem, and where each one wins. The table below pulls the most relevant 2026 figures into one view.

| Feature | Apple Pay | Google Pay / Wallet |

| Launch year | 2014 | 2015 |

| Global active users (2026) | ~744 million | ~820 million |

| U.S. mobile wallet share | 57% | ~17% |

| Annual transaction volume | $8.7 trillion | $5.2 trillion |

| Available in countries | 95 | 86 |

| Supported devices | iPhone, Apple Watch, iPad, Mac | Android phones, Wear OS, Chromebook |

| Banking partners | 11,000+ | Open Android ecosystem |

| Strongest market | United States | India, Southeast Asia, Africa |

| BNPL feature | Apple Pay Later | Pilot programs in select markets |

Table 2: Head-to-head feature and reach comparison (Sources: Chargeflow, CoinLaw, Worldpay 2026 reports).

Beyond the Big Two: PayPal, Samsung Pay, and Regional Giants

PayPal and Venmo

PayPal still owns the online checkout button. With around 210 million active users globally and roughly 47% of the U.S. online payment services market, PayPal remains the most-used digital wallet for web purchases. Its Venmo brand processed $342 billion in payment volume in 2025, dominating peer-to-peer payments among American Millennials and Gen Z. The PYUSD stablecoin, launched in 2023, hit a market cap of nearly $4 billion in 2025 as PayPal pushed deeper into crypto rails.

Samsung Pay and Cash App

Samsung Pay carved out a niche by supporting older magnetic-stripe terminals through Magnetic Secure Transmission technology, though its market share has settled around 34 million users worldwide. Cash App, owned by Block, has become the everyday spending tool for over 50 million U.S. users, especially in lower-income demographics where it functions as a quasi-bank. About 24% of U.S. consumers use Cash App regularly.

Alipay and WeChat Pay

In China, the conversation looks completely different. Alipay and WeChat Pay together hold over 90% of the local digital wallet market. WeChat Pay alone has more than 600 million active users. These platforms are super-apps. They handle payments, social messaging, ride-hailing, food delivery, and government services in a single interface. The closest Western equivalent does not exist yet, though Apple, Google, and PayPal are all inching in that direction.

What’s Next: Five Forces Reshaping Digital Wallets

Figure 3: The next wave of digital wallet evolution through 2030.

Stablecoins and Central Bank Digital Currencies

The biggest near-term shift is the rise of stablecoins inside mainstream wallets. After the U.S. passed the GENIUS Act in 2025 and Europe rolled out its MiCA framework, regulated stablecoins like USDC and PayPal’s PYUSD are increasingly used for cross-border payments and instant settlement. Stablecoin transaction volume crossed $4 trillion in just the first seven months of 2025. Meanwhile, China expanded its e-CNY digital yuan to pay interest on wallet balances starting January 2026, the first central bank digital currency to do so. Expect more wallets to natively support fiat, stablecoins, and CBDCs side by side.

Multi-Biometric Authentication

Single-factor biometrics like Face ID will not be enough as fraud gets more sophisticated. The next generation of wallets is moving to multi-biometric authentication, layering facial recognition, fingerprint scans, voice prints, and even palm vein patterns. Edge AI models running on the device analyze transactions in milliseconds, scoring behavior and device signals to flag suspicious activity before the payment clears.

Wearable Payments and Ambient Commerce

Wearable payments are growing roughly 19% year over year. Smartwatches lead the pack, but smart rings, fitness bands, and even smart glasses are entering the mix. The convenience matters most in high-frequency, low-friction settings. Think transit gates, gym entries, and stadium concessions. Apple Watch is now integrated with 75 metro systems globally.

Agentic Commerce and AI-Powered Wallets

This is the wild card. Agentic commerce describes a future where your AI assistant searches for deals, negotiates prices, and completes purchases on your behalf using stablecoins or tokenized assets that move instantly between machines. Early experiments are already running, and the wallet of 2030 may look less like an app you tap and more like a permission layer your AI agent calls. For a thoughtful look at where the regulation is heading, the

Bank for International Settlements has published guidance on the systemic implications of agentic finance and tokenized money.

Tokenized Real-World Assets

The line between a digital wallet and an investment account is blurring fast. Tokenization platforms now let users hold fractional ownership of real estate, private equity funds, fine art, and even music royalties in the same app where they store credit cards. Major institutions like Fidelity and Robinhood are leaning into this trend, pushing financial inclusion by lowering the entry bar for asset classes that were once locked behind accredited-investor gates.

The Road Ahead Is Not Without Bumps

None of this growth is guaranteed. Privacy concerns are rising, with 68% of consumers globally worried about how their spending data is collected and used. Cross-border payment fraud topped $50 billion in confirmed losses in 2025. Regulators in Europe and the U.S. are tightening rules around what wallet providers can do with consumer data, and bank-led alternatives like Paze are challenging Apple and PayPal for share.

There is also the question of small-business adoption. Only 57% of North American small businesses currently accept digital wallets, and just 12% accept cryptocurrency. Closing that gap will be one of the biggest commercial opportunities of the next five years.

Conclusion: The Wallet Is the New Operating System for Money

The rise of digital wallets is no longer a story about replacing cash. It is a story about replacing the entire stack between you and your money. Apple Pay perfected the tap. Google Pay scaled it across the Android world. PayPal owns the web checkout. Alipay and WeChat Pay turned the wallet into a super-app. The next chapter, written in stablecoins, biometrics, wearables, and AI agents, will go further still.

For consumers, the practical takeaway is simple. If you have not set up a digital wallet yet, do it. The security is better than plastic, the convenience is unmatched, and the ecosystem will only keep expanding. For merchants, ignoring digital wallet acceptance in 2026 is leaving real money on the table. And for everyone watching, the message is louder than ever. The wallet is the platform. Whoever owns the wallet owns the customer relationship of the next decade.

Frequently Asked Questions

Is Apple Pay or Google Pay safer to use?

Both Apple Pay and Google Pay use tokenization and biometric authentication, which makes them significantly safer than physical credit cards. Neither platform shares your actual card number with merchants. Apple’s tightly controlled iOS environment is often cited as marginally more secure, but Google Pay’s open architecture has matured significantly with on-device fraud detection. For everyday transactions, either is a strong choice.

Can I use Apple Pay and Google Pay in the same place?

Almost always, yes. Both wallets use the NFC contactless payment standard. If a merchant terminal accepts one, it almost always accepts the other. In the United States, more than 90% of retailers now support contactless payments, and the same goes for most of Europe, Australia, and urban Asia.

What happens if I lose my phone?

This is one of the strongest arguments for using a digital wallet. Apple Pay requires Face ID, Touch ID, or a passcode for every transaction, so a thief who picks up your phone cannot simply tap to pay. You can also remotely suspend or wipe your wallet through Find My iPhone or Google’s Find My Device. Compare that to losing a physical wallet, where a thief can swipe your contactless card before you even notice.

Will stablecoins and CBDCs replace traditional digital wallets?

They are more likely to be added to existing wallets than to replace them. The wallets you already use are increasingly being upgraded to support stablecoins like USDC and PYUSD, and central bank digital currencies in countries that issue them. Think of it as new payment rails being plugged into the same familiar app, rather than a wholesale change to a different product category.

Suggested Reading

• Worldpay Global Payments Report 2026 — the industry-standard annual breakdown of how the world pays.

• Capital One Shopping Research: Digital Wallet Statistics — comprehensive consumer adoption data for the U.S. market.

• World Economic Forum: Digital Assets in 2026 — long-view analysis of where tokenization and CBDCs are headed.

{ “@context”: “https://schema.org”, “@graph”: [ { “@type”: “BlogPosting”, “@id”: “https://yoursite.com/rise-of-digital-wallets#article”, “headline”: “The Rise of Digital Wallets: Apple Pay, Google Pay, and What’s Next”, “description”: “A 2026 deep dive into how digital wallets like Apple Pay and Google Pay reached 5.2 billion users, plus what stablecoins, wearables, and AI-powered agentic commerce mean for the future of mobile payments.”, “image”: [ “https://yoursite.com/images/digital-wallets-global-growth.png”, “https://yoursite.com/images/apple-pay-vs-google-pay-2026.png”, “https://yoursite.com/images/future-of-digital-wallets-trends.png” ], “datePublished”: “2026-04-28”, “dateModified”: “2026-04-28”, “author”: { “@type”: “Person”, “name”: “Author Name”, “url”: “https://yoursite.com/author/author-name” }, “publisher”: { “@type”: “Organization”, “name”: “Your Publication”, “logo”: { “@type”: “ImageObject”, “url”: “https://yoursite.com/logo.png” } }, “mainEntityOfPage”: { “@type”: “WebPage”, “@id”: “https://yoursite.com/rise-of-digital-wallets” }, “keywords”: “digital wallets, Apple Pay, Google Pay, mobile payments, contactless payments, NFC, stablecoins, CBDC, biometric authentication, fintech, tokenization, Apple Wallet, Google Wallet, PayPal, Venmo, Alipay, WeChat Pay, Samsung Pay, wearable payments, agentic commerce”, “articleSection”: “Fintech”, “wordCount”: 1750, “inLanguage”: “en-US”, “about”: [ { “@type”: “Thing”, “name”: “Digital wallet” }, { “@type”: “Thing”, “name”: “Mobile payment” }, { “@type”: “Thing”, “name”: “Contactless payment” } ], “mentions”: [ { “@type”: “Product”, “name”: “Apple Pay”, “brand”: { “@type”: “Brand”, “name”: “Apple” } }, { “@type”: “Product”, “name”: “Google Pay”, “brand”: { “@type”: “Brand”, “name”: “Google” } }, { “@type”: “Product”, “name”: “PayPal” }, { “@type”: “Product”, “name”: “Venmo” }, { “@type”: “Product”, “name”: “Alipay” }, { “@type”: “Product”, “name”: “WeChat Pay” }, { “@type”: “Product”, “name”: “Samsung Pay” } ] }, { “@type”: “FAQPage”, “@id”: “https://yoursite.com/rise-of-digital-wallets#faq”, “mainEntity”: [ { “@type”: “Question”, “name”: “Is Apple Pay or Google Pay safer to use?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Both Apple Pay and Google Pay use tokenization and biometric authentication, which makes them significantly safer than physical credit cards. Neither platform shares your actual card number with merchants. Apple’s tightly controlled iOS environment is often cited as marginally more secure, but Google Pay’s open architecture has matured significantly with on-device fraud detection. For everyday transactions, either is a strong choice.” } }, { “@type”: “Question”, “name”: “Can I use Apple Pay and Google Pay in the same place?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Almost always, yes. Both wallets use the NFC contactless payment standard. If a merchant terminal accepts one, it almost always accepts the other. In the United States, more than 90% of retailers now support contactless payments, and the same goes for most of Europe, Australia, and urban Asia.” } }, { “@type”: “Question”, “name”: “What happens if I lose my phone?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “Apple Pay requires Face ID, Touch ID, or a passcode for every transaction, so a thief who picks up your phone cannot simply tap to pay. You can also remotely suspend or wipe your wallet through Find My iPhone or Google’s Find My Device. Compare that to losing a physical wallet, where a thief can swipe your contactless card before you even notice.” } }, { “@type”: “Question”, “name”: “Will stablecoins and CBDCs replace traditional digital wallets?”, “acceptedAnswer”: { “@type”: “Answer”, “text”: “They are more likely to be added to existing wallets than to replace them. The wallets you already use are increasingly being upgraded to support stablecoins like USDC and PYUSD, and central bank digital currencies in countries that issue them. Think of it as new payment rails being plugged into the same familiar app, rather than a wholesale change to a different product category.” } } ] } ] }