It is the hottest week of the summer. A homeowner calls because the air conditioner finally quit. Your technician arrives, runs the diagnostics, and delivers the verdict: the system is done. It needs a full replacement. The customer nods. They know it is coming. Then they hear the number. The room goes quiet.

That silence costs HVAC companies real money every single day. The homeowner did not say no to the equipment. They said no to writing a check for thousands of dollars on the spot. This is the central problem that HVAC financing options for customers are built to solve. And the best part is that you can solve it without ever lending a dollar of your own money or turning your shop into a bank.

This guide breaks down how modern HVAC companies offer financing on $6,000 to $12,000 replacements. You will see how the money moves, what it costs you, and how to roll it out the right way.

Why Sticker Shock Stalls HVAC Replacement Sales

HVAC is unique in the home services industry. No one ever expects to buy a new furnace. It’s usually the result of an emergency situation. Homeowners need the system now and can’t wait for it to be convenient to buy.

Complete system change-outs are expensive. System replacement costs range from $6,000 to $12,000 on the low end and over $15,000 for higher efficiency systems. The cost will vary based on the efficiency of the equipment, install complexity, and local labor costs. This is a significant amount of money, especially for most households, and customers are not able to afford it all up front.

This naturally leads to customers stalling the sale. Customers will try to negotiate the sale by requesting cheaper systems, request repairs to extend the life of the system, and then just wait. The reality is that the customer most likely wants the system, but does not want to pay the price. This is the exact problem that offering financing would solve.

Typical installed replacement costs help you frame financing accurately.

| Project type | Typical installed cost | Why the range moves |

| AC unit replacement | $5,000 – $9,000 | SEER rating, tonnage, ductwork condition |

| Furnace replacement | $4,500 – $9,500 | Fuel type, efficiency (AFUE), venting |

| Full system (AC + furnace) | $8,000 – $14,000 | Matched system, install complexity |

| High-efficiency heat pump | $9,000 – $16,000+ | Cold-climate spec, electrical upgrades |

Ranges are illustrative U.S. averages; quote your local pricing for accuracy.

HVAC Financing Options for Customers: The Core Idea

Offering financing to your clients doesn’t mean you’re fronting the cost of the work yourself. You’re not. You partner with a third-party financing solutions provider. And in this model, the homeowner actually borrows the money. Your only job is to pitch the model and help the homeowner complete the necessary application.

You can think of this model similar to a car dealership. The dealership sells the car and helps you complete the loan paperwork, but they don’t provide the money to buy the car — the bank does. More and more HVAC contractors are adopting this model. The lender takes the credit risk. You get paid and get to move on to your next client.

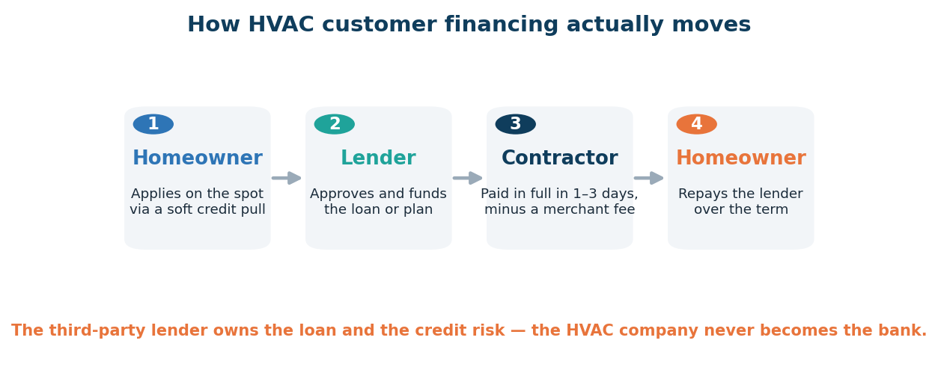

How Contractors Offer Financing Without Becoming a Bank

The mechanics are simpler than they look. Once a homeowner gets approved, the lender usually pays you the amount for the project within one to three business days of the job completion. The lender keeps a small percentage of the amount as a fee. The homeowner repays the lender over the term agreed upon. Once the funds are transferred to your account, you are completely out of the money loop.

The four-step flow of point-of-sale financing for contractors.

Since the lender owns the loan and the collections process, your exposure is nearly zero. You get paid in full and the homeowner liaises with the lender to settle the repayment. This separation is what allows you to provide financing for home services without having to bear the banking risk, the worry of being licensed, or absorption of losses from defaults.

Point of Sale Financing for Contractors: How the Money Actually Moves

Point of sale financing for contractors means that the entire process occurs in the homeowner’s living room, or wherever the sale occurs. The technician or comfort advisor simply pulls out a tablet or a phone. The homeowner inputs some information and there is a soft credit pull that results in a decision in mere seconds or minutes with no impact on the homeowner’s credit score for prequalification.

If the customer is approved, the customer chooses their plan and signs the agreement digitally. The plan gets installed and the lender wires the funds to your account. Everything happens in one sales appointment, which is the primary reason for such high conversion rates. There is no traveling to the bank, no days long waiting periods for decisions and no second appointment.

Speed is the most important feature of this type of financing. A furnace fails in the winter. The life and safety of the homeowners and their families is of primary concern. If you can resolve the problem the same day with an on the spot approval, you will not lose the job to a financing competitor.

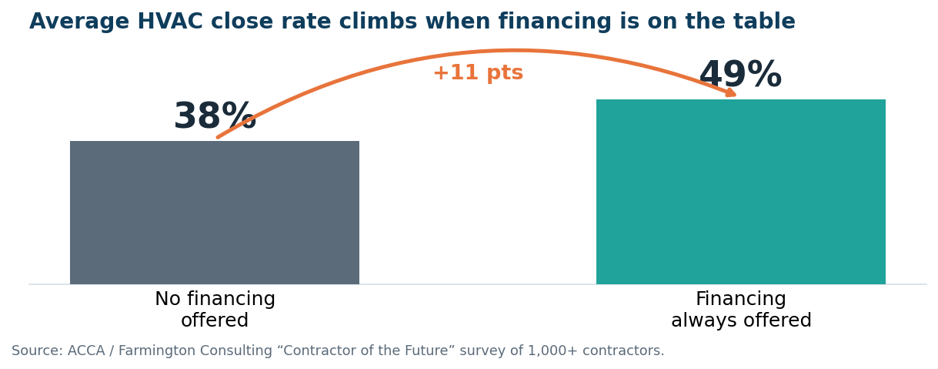

The Business Case: What Financing Does to Close Rates

This is where the data gets convincing. Financing is more than just an offering. It is an essential component of a sales strategy to improve close rates, average sale amount, and the range of equipment sold. Benchmarks that lenders publish typically show a 20% to 30% increase in close rates or the value of a project when financing is offered. However, always validate the results for a single vendor against your own.

Industry survey data shows a clear close-rate gap between contractors who offer financing and those who do not.

Independent survey data corroborates this. The Air Conditioning Contractors of America found average close rates of 38% for contractors not offering financing and a close rate of 49% for contractors that offer financing. Of the contractors that offer financing, those that mention financing always finance more of their replacement contracts than those that mention financing occasionally.

There is a framing effect to consider as well. Of the contractors that financing was suggested to them, those that preceded their offer with a monthly payment rather than the total price, found that financing about 100% of the time. In addition, they were less likely to sell a base model and more likely to sell premium, high-efficiency systems. A homeowner that is concerned about the total cost of the sale equating to $9,000, will likely approve of the sale with the added offer of a warranty when presented with a $9,000 sale with a $100/month offer.

Understanding the Merchant Discount (the Real Cost to You)

Project financing creates an illusion of a cost-free deal to the borrower, but this creates a considerable risk factor for the borrower. The lender charges a merchant discount (or dealer fee), which is a percentage of the total project cost. In practice, this fee generally ranges between 2% – 10%, depending on the length and terms of the promotion.

The reasoning behind this is quite simple. In a traditional installment loan, the borrower pays very little, which makes the loan attractive. In a long 0% promotional plan, the cost to the borrower is higher because the lender is essentially giving away interest. Consequently, this fee is absorbed by the borrower, and the cost of the promotion is related to the lender’s profit margin.

How promotional length tends to affect the merchant discount you pay.

| Plan offered to customer | Typical merchant fee | Who effectively pays the interest |

| Standard installment (interest-bearing) | ~2% – 4% | The customer, through APR |

| Short 0% / same-as-cash promo | ~3% – 6% | Mostly the customer; some cost to you |

| Long 0% promo (18–60 months) | ~6% – 10% | You, via a higher merchant discount |

Most contractors incorporate the anticipated cost of financing into their pricing. Retailers do the same with a cost of card processing. In reality, a higher close rate and a larger average ticket provides more than enough to cover the merchant discount. The math usually supports the use of financing.

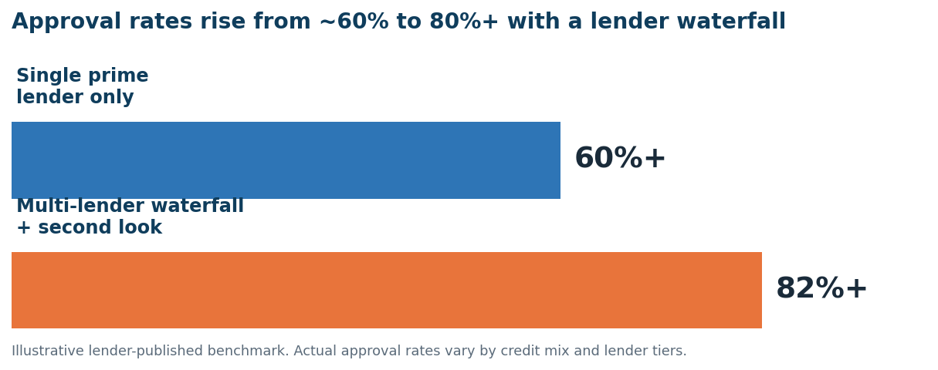

Waterfall and Second-Look Lending: Turning a “No” Into a “Yes”

The single-lender model is disastrous. Should the only lender at the top of the hierarchy say no, the deal is dead. The embarrassment caused to the homeowner, the frustration endured by the salesperson, and the opportunity that walks out the door, all due to a failed financing proposition, are just some of the inconveniences caused by single-lender schemes. Waterfall financing eliminates this problem.

Waterfall financing involves a single application moving through a pre-defined sequence of lenders. The first lender is, once again, the prime lender. Should that lender refuse, the application travels down the hierarchy to the next, or second look, lender, who would be within the near-prime tier. Should that lender also refuse the application, it then travels to the sub-prime tier. This is all done with the homeowner having to fill out a single application, and at no point having to re-apply. Unbeknownst to the homeowner, a number of lenders are competing to approve the deal.

Adding second-look tiers can lift overall funded approvals well past a single prime lender.

Approvals are impacted in an important way. If lenders follow benchmarks, a program that uses a single prime lender to approve 60% of applicants can use a multi-lender waterfall and second-look tier to approve 80% or more. With no new leads or marketing costs, every job funded at your average ticket becomes revenue.

Survey results back the trend. A significant portion of HVAC contractors that provide financing have second-look programs. In fact, many of these contractors have funded a greater proportion of replacement sales. Second-look programs ensure that homeowners in need of a functioning system are not turned away due to having subprime credit.

HVAC Payment Plans: The Main Types Explained

HVAC plans come in various arrangements, and knowing the differences can help your margin and your customer’s payment. Some structures include true 0% APR promotions, deferred interest “same-as-cash” offers, reduced-rate installment loans, and low-payment long-term loans. Each of these believes cost, approval, and monthly payment in a different way.

A side-by-side look at common HVAC payment plan structures.

| Plan type | How it works | Best fit |

| True 0% APR promo | No interest during the term, no retroactive charge if a balance remains afterward. | Strong-credit customers who want predictable payments. |

| Deferred-interest same-as-cash | No interest if paid in full by the deadline; otherwise interest is charged back to day one. | Customers expecting a tax refund or bonus to pay it off. |

| Reduced-rate installment | Fixed monthly payments at a set APR over 24–84 months. | Customers focused on a low, steady monthly number. |

| Low-payment long-term | Longer terms stretch payments down, total interest rises. | Budget-tight households needing the lowest payment. |

Offers featuring deferred interest should be considered more cautiously. While these offers may be more attractive to marketing teams, customers should not be lured in without understanding these offers. These promotions tend to have a deadline to pay off the balance or else interest will be charged for every day the customer has the balance since the purchase, and will be charged a few days prior to the payment deadline. The difference between deferred interest and a true offer of 0% interest is described clearly by the Consumer Financial Protection Bureau. It is worthwhile to understand the difference between the two offers to understand the consequences before choosing a plan.

Popular HVAC Financing Platforms and Lenders

Powering most HVAC and home-services financing are several established players. As terms and fees are subject to change, and so are lender networks, consider the descriptions below as preliminary and check with the providers for the most up to date offerings.

Synchrony

Synchrony is among the biggest providers of consumer and home-improvement financing in the U.S. of which home services and HOME card products are the most utilized financing solutions for HVAC promotions with deferred interest and reduced-rate plans. Many contractors operate Synchrony as a prime tier in an extended program.

GoodLeap

GoodLeap specializes in financing home improvements and sustainable upgrades including HVAC and heat pump systems. Their financing platform primarily consists of longer-term installment loans. Homeowners looking to take advantage of incentive programs to reduce the cost of and switch to higher efficiency systems are often motivated by the prospect of lower monthly payments.

Wisetack

Wisetack offers embedded buy-now-pay-later solutions to finance in-person home services. Wisetack is designed for fast mobile applications at the point of sale. Wisetack provides clear terms without deferred interest. Many contractors have a preference for Wisetack, due to issues of trust.

Service Finance Company

Service Finance Company provides specialized lending services for home improvement contractors for HVAC dealers in financing offered through manufacturer dealer programs. It lends equipment with promotional financing.

FinMkt and ServiceTitan

FinMkt offers a multi-lender waterfall platform that routes a single application to multiple lenders across the Prime, Near-Prime, and Sub-Prime categories to increase the chances of approval. ServiceTitan, a market-leading field-service software platform, offers a similar single-application waterfall via its TURNS integration. This allows contractors to process financing in the same platform they use for scheduling and invoicing.

How to Offer Financing for Home Services the Right Way

Implementing a program involves more than just completing a lender agreement. Contractors that win with financing consider this a sales discipline. Sales discipline means presenting replacement proposals as a payment rather than a total price. Simply pricing the replacement with a payment increases financing penetration and system sales. Sales discipline also means presenting financing for every job, not just presenting financing when the customer pushes back. Consistency is what differentiates the top financing sales contractors from the rest.

Training is critical, especially for technicians that feel awkward requesting financing; some technicians even feel embarrassed to present the financing request. This should not be the case. Presenting financing is a discipline, just like advertising. Think about every car commercial; they present the payment and never the price. Presenting financing should be a discipline for your team, and to assist with this discipline, provide your team with a mobile application for financing, a payment versus repair cost calculator, and simple scripts. A simple, short, and repeatable financing request should be the goal; if your team is not going to use a complex financing request, why should you train and practice for one?

The application you choose for financing should be designed for fieldwork. Considering your funding sales team works on the client’s job site, rather than at your offices, your application should be designed to work on mobile. Also, in the instance that your funding request is declined, choose a robust first-tier funding source with a second-tier funding source.

Compliance and Doing Right by the Customer

When you offer financing, you take on legal responsibilities. Good platforms take care of most of the necessary compliance for you. This includes dealing with Truth in Lending Act disclosures, sending adverse-action notices when an application is declined, and handling state licensing at the platform level. It’s still important for you to understand the compliance basics so your team can deliver the financing options in an honest manner.

You need to be given an opportunity to analyze every component of an offer (rates, fees, and terms). You need to disclose the consequences of failing to reach the payoff amount. You shouldn’t be financing to help homeowners make poor decisions on the purchase of an unnecessary system upgrade. Financing should not be used to trick homeowners into signing an agreement that they cannot understand. Financing programs that are based on trust will receive referrals. Financing programs that are based on a lack of understanding will receive complaints.

Conclusion

Your team can use the best HVAC financing options for customers so that $8,000 replacement doesn’t have to end in silence. With the facilitated loan, the risk-carrying lender, and the comfortable payment for the homeowner, your team can sign the agreement. Your team can suggest the monthly payment, use the financing on every job, and support your primary lender with a secondary look tier. This way, your team can win the job over competitors, losing the work to sticker shock. This can all be done without your team ever being a bank.

Frequently Asked Questions

Do HVAC companies lose money by offering financing?

Not usually. The lender applies a merchant discount of approximately 2% to 10% for each offer. Most contractors absorb that cost for the job, similar to how retailers absorb card processing costs. The increase in from the financing offer higher close rates and higher average receipts tends to produce net profit rather than loss.

Does offering financing make the contractor responsible if a customer stops paying?

No. The loan and the collection process are owned by the third-party lender. The contractor is paid in full and bears no credit risk. The lender is repaid directly by the homeowner. This is the exact reason contractor financing is offered without a contractor becoming a bank.

What credit score do customers need to qualify for HVAC financing?

It depends on the lender and the specific plan. Generally, preferred lenders will require stronger credit to qualify for 0% promotions. With a waterfall and second-look program, near-prime and subprime tiers can approve the financing for homeowners with lower credit scores. This is how the average approval rate for most lenders increases from 60% to about 80% or more. Many homeowners with less than perfect credit can still qualify for a workable credit plan.

How fast does the contractor get paid after a financed job?

Speed is of the essence with point-of-sale lending. Most lenders disburse funds to the contractor within one to three business days after the job completion verification. The homeowner pays back the lender during the agreed loan term. That fast funding fits perfectly into the HVAC sales cycle.