As businesses expand, their financial systems must evolve too. Payment processes that once worked for a few hundred transactions may struggle when faced with thousands daily. If your company is scaling fast, the key to sustainable growth lies in upgrading your business payments infrastructure — not just patching it.

This guide explains how to future‑proof your payment architecture, manage global transactions efficiently, and ensure security and reliability as your volume spikes.

Why Scaling Payments Infrastructure Matters

Strong payments infrastructure creates the backbone of growth. Manual systems and traditional gateways can become a bottleneck as transaction volume and complexity rise. Poor scalability leads to delayed payments, failed integrations, and revenue leakage.

A scalable payments system keeps cash flow steady, improves customer experience, and provides the flexibility to expand into new markets without friction.

| Scaling Factor | Impact on Payments | Common Issues if Unoptimized |

|---|---|---|

| Transaction Volume | Increased processing demand | Delays, failed charges |

| Multi‑Currency Operations | Global expansion | FX errors, poor conversion rates |

| New Payment Methods | Customer convenience | Fragmented user experience |

| Compliance Requirements | Regulatory change | Risk of violation penalties |

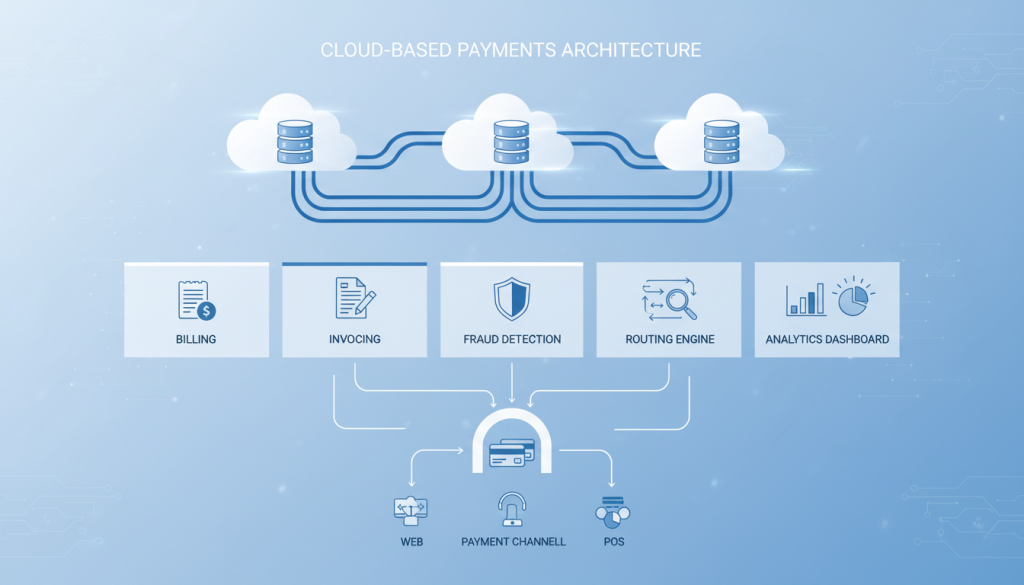

Building a Scalable Payment Architecture

Scaling payments isn’t just about processing more transactions. It’s about creating a modular, API‑driven ecosystem that can adapt as your business grows.

Modular Architecture

A modular design separates functions like billing, invoicing, reconciliation, and fraud detection. This makes it easier to scale and integrate new technologies without disrupting your core systems.

API‑Driven Integrations

Modern businesses rely on API‑first payment solutions to connect gateways, accounting systems, and CRMs seamlessly. APIs allow real‑time data syncing, automatic reconciliation, and faster settlement times.

Cloud‑Based Infrastructure

Cloud environments such as AWS, Google Cloud, and Microsoft Azure enable dynamic scaling — allowing capacity to expand or contract in real time. This flexibility minimizes downtime during high‑volume periods like holidays or product launches.

Choosing the Right Payment Processor

Different processors offer unique advantages, from global reach to advanced security. Selecting the right one determines how well your payment infrastructure can grow.

Stripe

Stripe provides an advanced developer‑friendly API, making it perfect for businesses that prioritize customization and global connectivity. The platform supports 135+ currencies and a wide range of alternative payment methods.

PayPal

PayPal simplifies consumer trust and offers strong fraud detection algorithms. It’s ideal for e‑commerce brands looking for instant credibility and broad market acceptance.

Adyen

Adyen provides enterprise‑grade omnichannel payment processing, supporting both online and in‑store transactions. Powerful risk management tools help larger merchants scale with confidence.

For an in‑depth comparison of modern payment processors, see NerdWallet’s review of best payment gateways.

Automating Payment Workflows

Automation is the key to maintaining operational efficiency as transaction volumes grow. By integrating automation into invoicing, reconciliation, and reporting, you reduce human error and save labor hours.

When scaling, leverage automated payment routing and intelligent transaction retries to reduce declines. Machine learning algorithms can analyze customer behavior and predict which payment methods yield the highest success rates.

Example: A subscription SaaS provider can use automated systems to trigger renewals, retry failed cards, and reconcile payments daily without manual oversight.

Managing Global Transactions and Multi‑Currency Systems

Once your business crosses borders, payment processing becomes more complex. Each region has its own regulations, preferred payment methods, and currency conversion rates.

To succeed globally, integrate payment networks that support regional payment preferences (like SEPA in Europe or UPI in India). Also, use multi‑currency accounts to hold local balances and prevent unnecessary FX conversions.

| Region | Preferred Payment Method | Processing Challenge |

|---|---|---|

| North America | Credit/Debit Cards | Chargeback management |

| Europe | SEPA, iDEAL | Multi‑currency reconciliation |

| Asia | Mobile Wallets, UPI | Local compliance |

| Latin America | Cash‑based Vouchers | Settlement delays |

Ensuring Security and Compliance

Regulatory requirements evolve rapidly, and compliance is a non‑negotiable pillar of any scalable payments infrastructure. From PCI DSS standards to GDPR and AML/KYC protocols, maintaining compliance ensures long‑term viability.

Encrypting sensitive data, implementing tokenization, and using two‑factor authentication reduce fraud risks. Periodic audits and automated monitoring can detect and prevent suspicious activities before they escalate.

Visit PCI Security Standards Council for updated compliance information and frameworks.

Data Insights and Reporting for Growth

Data is the hidden currency of scaling. As your payment ecosystem grows, tracking metrics like authorization rates, chargeback ratios, and settlement time becomes essential. Use analytics dashboards to identify weak points and opportunities for optimization.

Machine learning tools can predict churn, forecast cash flow, and highlight regions with higher transaction success rates. This level of visibility allows financial teams to make informed decisions about pricing, localization, and investment.

The Role of Artificial Intelligence in Payment Scaling

AI is becoming central to smart payment routing and fraud detection. Instead of using static rules, machine learning algorithms continuously learn from transaction patterns. AI not only identifies risk but also dynamically routes payments through the most efficient processors, reducing transaction costs.

For growing enterprises, implementing AI‑based payments intelligence ensures higher success rates and smoother customer experience without constant human intervention.

Integrating Payments With Back‑Office Systems

To maintain healthy financial operations, payments must connect seamlessly with accounting, ERP, and CRM platforms. Integration with tools like QuickBooks, Xero, or Oracle NetSuite ensures real‑time synchronization of invoices and settlements.

Unified data flows reduce reconciliation times, minimize mismatched transactions, and improve audit readiness. This connected back‑office approach drives transparency across departments and simplifies financial reporting during audits or mergers.

Supporting New Payment Methods and Alternative Channels

Customers expect flexibility. As your business scales, offering digital wallets, Buy Now, Pay Later (BNPL) options, and cryptocurrency payments can attract wider demographics.

Supporting innovations such as Apple Pay, Google Pay, or regional wallets builds convenience and trust. However, every new payment channel requires secure API integrations and dynamic risk assessment to maintain compliance.

How Infrastructure Upgrades Boost Cash Flow Efficiency

Every delay in payment settlement affects your working capital. Upgrading your systems reduces these delays and increases real‑time visibility. With faster settlement cycles and reduced manual intervention, you keep capital flowing smoothly across departments.

This financial agility can make the difference between steady growth and operational friction.

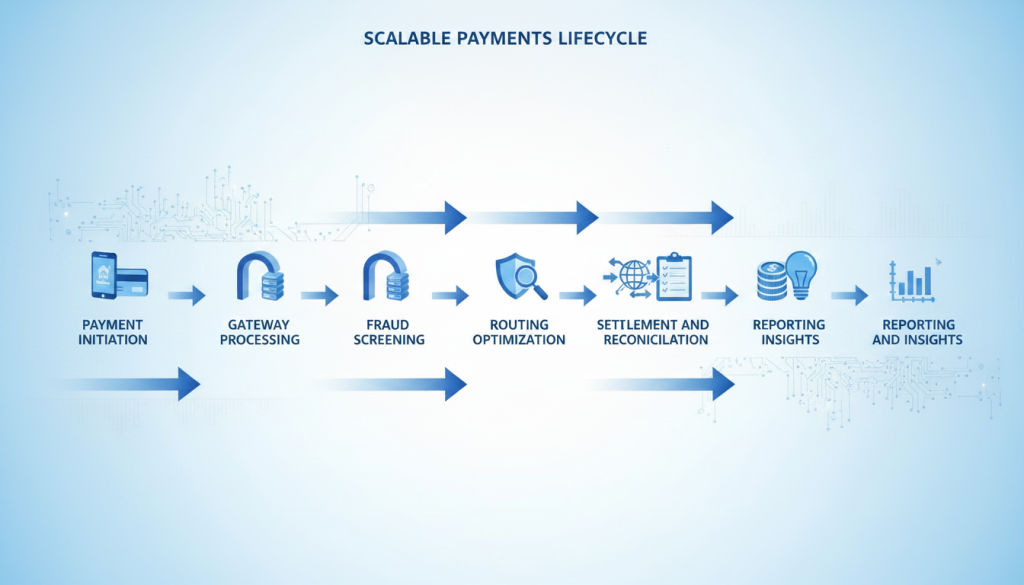

Infographic: The Lifecycle of Scalable Payments

Each stage expands with volume and intelligence as infrastructure evolves.

Overcoming Common Scaling Challenges

When companies scale payments, a few roadblocks often appear: integration issues, latency during high loads, or unexpected fees. The solution lies in selecting partners that grow with your business and implementing proactive monitoring systems.

Establishing redundant gateways and automated failovers ensures uninterrupted service even when one provider experiences downtime. Regular load testing helps predict peak performance thresholds before real issues occur.

Measuring Success After Scaling

Success isn’t only measured in speed but also in reliability and customer satisfaction. Track metrics like transaction approval rates, API uptime, and international payment success rates. Organizations with resilient infrastructure often see improved cash flow predictability, higher customer retention, and reduced operational costs.

| Metric | Before Scaling | After Scaling | Improvement |

|---|---|---|---|

| Average Transaction Time | 5.2 seconds | 1.8 seconds | 65% Faster |

| API Downtime (Monthly) | 4 hours | < 30 minutes | 87% Reduction |

| Payment Success Rate | 91% | 98.5% | +7.5% |

| Chargeback Ratio | 2.1% | 0.8% | -61% |

Conclusion

Scaling your business payments infrastructure is not just a technical upgrade — it’s a strategic step toward financial resilience. By investing in modular architecture, cloud‑based systems, and AI‑powered automation, companies can handle massive transaction volumes while maintaining security and compliance.

Your payments ecosystem should grow with your business — faster, smarter, and more connected every step of the way.

Frequently Asked Questions (FAQs)

1. What is payment infrastructure scalability?

It refers to how efficiently your payment systems can handle growing transaction volumes, new payment methods, and global expansion without breaking or slowing down.

2. How can a small business start scaling payments early?

Adopt API‑based payment gateways and cloud services that allow modular expansion. Start small but ensure compatibility with enterprise‑level solutions.

3. Are cloud‑based payment systems secure?

Yes. Major cloud providers follow strict compliance frameworks. Combined with encryption, tokenization, and ongoing audits, they offer enterprise‑grade security.

4. What role does automation play in scaling payments?

Automation streamlines repetitive tasks like invoicing, reconciliation, and fraud detection, allowing your finance teams to focus on strategy and business growth.