Most signed it quickly. Many regretted it slowly. That slow regret usually starts the moment the first monthly statement arrives and the numbers don’t add up to what the sales rep promised.

Merchant services agreements are among the most complex contracts small businesses encounter. They are written by legal teams that work for processors, not for you. They contain dozens of clauses, addenda, and buried terms that can lock you into unfavorable rates, steep penalties, and years of automatic renewals. The good news? The red flags are almost always the same. Learn to spot them before you sign, and you will save yourself thousands of dollars and months of frustration.

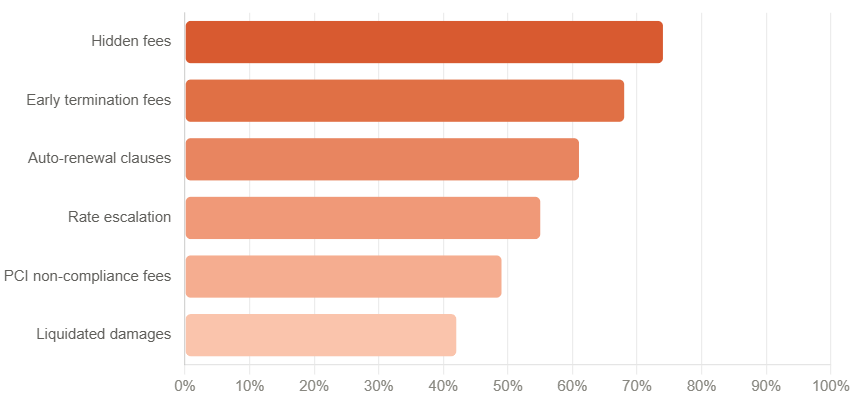

% of merchant complaints linked to each contract red flag (source: industry surveys)

This guide walks you through the most important warning signs to look for in any merchant services contract, along with the questions you should ask and the terms you should never accept.

Table of Contents

Understanding the Structure of a Merchant Services Contract

Before diving into red flags, it helps to understand what you are actually signing. A merchant services contract is rarely a single document. It is typically a package that includes a merchant application, a program guide or terms and conditions document, an equipment agreement if you are leasing a terminal, and any addenda tied to specific services like gateways or POS software.

Processors bank on the fact that most business owners focus on the application and ignore the program guide. That program guide is where the dangerous terms live. Always request every document before signing and read all of them carefully. If a provider refuses to give you the full terms ahead of signing, walk away immediately.

Red Flag #1: Vague or Inflated Rate Structures

Processing rates should be transparent and clearly defined. The cleanest pricing model is called interchange-plus pricing, where you pay the card network’s wholesale interchange rate plus a fixed markup by the processor. This model is honest and auditable.

The first red flag appears when a contract uses tiered pricing instead. Tiered pricing groups transactions into buckets — qualified, mid-qualified, and non-qualified — without clearly defining which transactions fall into each tier. In practice, this allows processors to quietly downgrade most of your transactions to higher-rate tiers, inflating your effective cost without technically lying about your rate. If a contract quotes you a single rate like 1.79% but buries language about tiered pricing in the program guide, that quoted rate may apply to only a fraction of your actual transactions.

Look for contracts that state your exact markup above interchange, fully disclose all per-transaction fees, and provide a sample statement so you can verify the math before you are locked in.

Red Flag #2: Early Termination Fees and Liquidated Damages

One of the most financially damaging clauses in a merchant services contract is the early termination fee, or ETF. A reasonable ETF is a flat fee, typically under $300, charged if you cancel before your contract term ends. Many merchants consider this acceptable in exchange for a lower rate.

The red flag appears when the ETF is calculated as liquidated damages. This means the processor estimates how much profit they would have made for the remaining months of your contract and charges you that full amount as a penalty for leaving. A business processing $50,000 per month that tries to exit a three-year contract with 18 months remaining could face an ETF in the tens of thousands of dollars under a liquidated damages clause. Always ask for the ETF to be expressed as a fixed dollar amount. If the provider refuses, treat it as a serious warning sign.

Red Flag #3: Long Contract Terms with Automatic Renewal Clauses

A standard merchant services agreement runs for one to three years. That alone is not a problem, provided the rates are fair and the exit terms are reasonable. The problem compounds when the contract includes an automatic renewal clause that is buried deep in the fine print.

These clauses automatically roll your contract into a new term — often at the same length as the original — unless you provide written cancellation notice within a very specific window. That window is typically 30 to 90 days before the renewal date. Miss the window by a single day and you are locked in for another two or three years with the same early termination penalties applying all over again.

Always negotiate to have automatic renewal clauses removed entirely. If the processor insists on keeping them, ensure the cancellation window is at least 90 days and that you receive written notification 60 days before that window opens.

Red Flag #4: Hidden and Junk Fees

Beyond the processing rate, merchant services contracts can contain a remarkable number of fees that are never mentioned during the sales process. These are sometimes called junk fees, and they accumulate quietly on your monthly statement. Common examples include monthly minimum fees, which charge you a set amount if your processing volume falls below a threshold. There are also statement fees, batch fees, annual fees, regulatory compliance fees, network access fees, and IRS reporting fees.

None of these fees are inherently illegal, but they become a red flag when they are not clearly disclosed before signing. A contract that quotes a low processing rate but layers on $75 or more in monthly junk fees may cost more overall than a simpler contract with a slightly higher rate. Ask every provider for a complete fee schedule in writing and compare total monthly cost, not just the headline rate.

| Fee type | Fair / reasonable range | Predatory / red flag range |

| Early termination fee | $0 – $295 flat | $500 – $5,000+ or liquidated damages |

| Monthly minimum fee | $0 – $25/month | $50+/month or percentage-based |

| PCI compliance fee | $0 – $120/year | $20+/month with vague triggers |

| Processing rate | 1.5% – 2.9% (interchange-plus) | 3%+ flat or opaque tiered pricing |

| Contract length | Month-to-month or 1 year | 3–5 years with auto-renewal |

| Statement fee | $0 – $10/month | $25+/month bundled with other charges |

Typical vs predatory fee structures — what to expect

Red Flag #5: PCI Compliance Fees and Non-Compliance Penalties

Payment Card Industry Data Security Standard compliance, known as PCI DSS, is a genuine requirement for all businesses that accept card payments. Compliance involves completing an annual self-assessment questionnaire and, for larger merchants, third-party audits. It is a real obligation, and some processors legitimately charge a modest annual fee to help you manage it.

The red flag appears in two forms. First, some processors charge a monthly PCI compliance fee every month of the year for a service that is only an annual requirement. Second, they simultaneously charge a non-compliance fee if you have not completed your annual questionnaire. Both fees can run $20 to $30 per month, meaning a merchant who does not actively manage their compliance status can be charged over $500 per year in PCI-related fees for what should cost a fraction of that. Review any PCI language carefully and confirm exactly what you will be charged, when, and why.

Red Flag #6: Rate Increase Clauses

Some merchant services contracts include language that allows the processor to raise rates at any time with minimal notice. These clauses are sometimes framed as pass-through cost adjustments tied to card network changes, which is legitimate when it applies only to actual interchange increases. The red flag is language that allows the processor to raise its own markup unilaterally, with notice as short as 30 days.

A fair contract should distinguish clearly between interchange pass-through adjustments, which are outside the processor’s control, and markup changes, which are entirely within it. If the contract allows the processor to raise its markup for any reason with short notice and your only remedy is early termination — subject to an ETF — you have essentially no pricing protection at all.

Red Flag #7: Equipment Lease Agreements

Terminal leasing is one of the most profitable and problematic practices in the merchant services industry. A credit card terminal that retails for $200 to $400 can be leased through a non-cancellable equipment lease for $30 to $75 per month over 48 months, resulting in total payments of $1,440 to $3,600 for a device worth a fraction of that.

The word non-cancellable is the critical warning sign. Unlike the processing contract, an equipment lease is a separate financial agreement, often with a different company, and it cannot be terminated even if you cancel your merchant account. You will continue paying the lease for every remaining month regardless of whether you are using the equipment. Always purchase terminals outright. Reputable processors either sell them at cost or provide them free with a service agreement.

Red Flag #8: One-Sided Dispute and Chargeback Language

Chargebacks are an unavoidable part of accepting card payments. What varies significantly is how your contract defines your rights when disputes arise. Some contracts include clauses that allow processors to freeze your funds indefinitely during a chargeback investigation, hold reserves far in excess of what is reasonable, or terminate your account and withhold funds based on an internal risk assessment with no appeal process.

These clauses tend to be one-sided by design. Legitimate processors do need protections against high-risk merchants, but those protections should be proportionate and clearly defined. Look for specific language about how long funds can be held, what triggers a reserve, what the appeal process is, and whether you have the right to a written explanation for any account suspension.

A Practical Contract Review Checklist

Before signing any merchant services agreement, work through these questions systematically. First, confirm the pricing model is interchange-plus with a disclosed, fixed markup. Second, locate the early termination fee and verify it is a flat amount rather than liquidated damages. Third, find the auto-renewal clause and confirm the cancellation window. Fourth, request a complete fee schedule and add up total monthly costs. Fifth, review all PCI-related language and confirm the annual versus monthly billing structure. Sixth, confirm that any equipment you need is being purchased, not leased under a separate non-cancellable agreement. Seventh, review chargeback and fund-hold language and understand the appeal process.

If the provider is unwilling to answer any of these questions clearly and in writing before you sign, that reluctance is itself a red flag. Reputable processors have nothing to hide and will welcome a thorough review.

How to Protect Yourself Before Signing

The best time to negotiate a merchant services contract is before you need a payment processor urgently. Business owners switching providers under time pressure make poor decisions. Start your search early, get multiple quotes, and compare them on total cost, not rate alone.

Ask every provider for a sample statement from a comparable business so you can verify exactly how fees appear in practice. Request that all verbal promises made during the sales process be included in the written contract. If the sales representative says there are no hidden fees, ask them to add that in writing. If they refuse, the promise was never real.

Consider having a payment industry consultant or an attorney review any contract with estimated monthly fees of $500 or more. The cost of a professional review is almost always less than the cost of a bad contract. Resources like the

You can learn more from resources like the Electronic Transactions Association (ETA) and the Consumer Financial Protection Bureau (CFPB), which provide free guidance on payment processing rights and industry standards.

Conclusion

Merchant services contracts are not written to be easy to read. They are long, dense, and full of language that protects the processor rather than your business. But the red flags are consistent and learnable. Vague pricing, excessive termination fees, automatic renewals with short cancellation windows, undisclosed junk fees, PCI billing traps, non-cancellable equipment leases, and one-sided dispute clauses appear again and again across bad contracts.

You do not need a law degree to protect yourself. You need patience, the right questions, and the willingness to walk away from any provider that will not give you straight answers. The payment processing industry is competitive. Fair, transparent providers exist in every market segment. Give your business the time it deserves to find one.

Frequently Asked Questions

1. What is the average early termination fee for a merchant services contract?

Early termination fees typically range from $0 to $500 for flat-fee contracts. However, contracts with liquidated damages clauses can result in ETFs of several thousand dollars or more, depending on your processing volume and the remaining contract term. Always verify the exact ETF structure before signing.

2. Can I negotiate the terms of a merchant services agreement?

Yes, and you should. Many processors — especially independent sales organizations — have flexibility on ETFs, contract length, and monthly fees. The rates themselves are often less negotiable, since they reflect underlying interchange costs, but you can frequently negotiate the contract term down to one year and cap or eliminate the early termination fee with some persistence.

3. Is tiered pricing ever acceptable in a merchant services contract?

Tiered pricing is not inherently fraudulent, but it is structurally opaque and nearly always more expensive than interchange-plus pricing for merchants with moderate to high card volumes. If a provider only offers tiered pricing, push for a detailed breakdown of which transaction types fall into each tier before agreeing to any rate.

4. What should I do if I am already locked into a bad merchant services contract?

Start by documenting all fees and comparing them against your original agreement. If you find undisclosed charges, file a complaint with your state attorney general’s office and the CFPB. Contact a payment industry attorney to assess whether any contract terms are unenforceable in your state. In some cases, processors will negotiate an early exit rather than face a regulatory complaint. If all else fails, calculate the total cost of exiting early against the ongoing cost of the bad contract and choose the lower number.

Published April 2026 | For informational purposes only. Consult a payment industry professional or attorney for advice specific to your business.