Every time a customer swipes, taps, or types their card, a fee disappears from your revenue. Most business owners accept this silently. But few realize that the pricing model their processor uses — not just the rate can mean the difference between paying thousands more or less per year. Two models dominate the market: interchange-plus pricing and flat-rate pricing. Choosing the wrong one for your business size and card mix is one of the most common and costly mistakes in merchant services.

This guide breaks down exactly how each model works, when each one wins, and how to calculate which pricing structure fits your business today and as you grow.

What Is Interchange, and Why Does It Matter?

Before comparing the two pricing models, it helps to understand the foundation they share: interchange fees. Every time a customer pays by card, the card networks — Visa, Mastercard, American Express, and Discover — collect a fee called interchange. This fee primarily goes to the card-issuing bank to compensate for fraud risk, rewards programs, and processing infrastructure. Interchange rates are set by the card networks themselves, and they are not negotiable for merchants.

What is negotiable is the markup your payment processor adds on top. That markup is where interchange-plus and flat-rate pricing diverge completely.

Interchange rates vary significantly depending on the card type used. A basic debit card might carry an interchange rate of just 0.05% + $0.22. A premium travel rewards credit card can carry a rate of 2.3% or higher. Corporate purchasing cards sit even higher. This variance is critical to understanding which pricing model benefits your specific business.

What Is Interchange-Plus Pricing?

Interchange-plus pricing — also called cost-plus pricing — is a transparent model where you pay the actual interchange rate charged by the card network, plus a fixed markup that your processor keeps. For example, if the interchange rate on a transaction is 1.65% and your processor’s markup is 0.20% + $0.10, your total cost for that transaction is 1.85% + $0.10. No bundling, no guessing.

The core advantage of this model is transparency. Your monthly statement shows every card type, every interchange category, and the processor’s margin in plain view. This makes it straightforward to audit costs, switch processors, and spot anomalies. It also means your costs move with reality — when a customer pays with a low-cost debit card, you pay a lower rate automatically.

The downside is complexity. Interchange-plus statements can run several pages long with dozens of interchange categories. If your team is not equipped to read them, the data becomes noise rather than insight. There is also the issue of variability — because your costs depend on which cards customers use, your monthly bill is harder to predict down to the dollar. However, for most growing businesses, the savings potential far outweighs the complexity.

What Is Flat-Rate Pricing?

Flat-rate pricing takes a radically different approach. Your processor charges a single percentage — and sometimes a per-transaction fee — on every transaction, regardless of the card type used. Popular processors like Square, Stripe, and PayPal have built their entire business models around this approach.

Square

Square charges 2.6% + $0.10 for in-person card-present transactions and 2.9% + $0.30 for online payments. No monthly fees, no interchange category complexity. Every transaction is treated the same way, from a debit card tap to a corporate Amex.

Stripe

Stripe charges 2.9% + $0.30 per online transaction as its standard rate. For in-person payments using Stripe Terminal, the rate drops to 2.7% + $0.05. Stripe also offers interchange-plus pricing for platforms using Stripe Connect, making it one of the few processors that gives businesses a genuine choice between both models.

PayPal

PayPal charges 3.49% + $0.49 for standard card transactions through its checkout and 2.29% + $0.09 for QR code-based in-person payments. PayPal’s flat-rate structure is straightforward but tends to be higher than competitors’ at similar volumes.

The appeal of flat-rate pricing is immediacy and simplicity. You always know exactly what each transaction costs. There is no learning curve, no multi-page statements, and no need to understand interchange categories. For a freelancer accepting occasional payments, or a startup that has not yet determined its payment mix, flat-rate pricing removes friction entirely.

The downside becomes apparent at scale: that flat percentage is set high enough for the processor to profit even on expensive rewards cards. When you use a debit card — which carries a much lower interchange rate — the processor pockets the difference as pure margin.

Side-by-Side Comparison

The table below summarizes the key differences between the two pricing models across the factors that matter most to most business owners.

| Factor | Interchange-Plus | Flat-Rate |

| Pricing Structure | Interchange rate + fixed markup | Single flat percentage rate |

| Transparency | Full — itemized per transaction | Opaque — bundled pricing |

| Cost at Low Volume | Higher effective rate possible | Predictable, easy to forecast |

| Cost at High Volume | Significantly cheaper | Can become expensive |

| Best Card Type Savings | Debit & basic credit cards | Rewards & corporate cards |

| Monthly Statements | Detailed breakdown | Simple single-line fees |

| Setup Complexity | Moderate — requires understanding | Very easy to get started |

| Best For | Scaling businesses, retailers | Startups, freelancers, low volume |

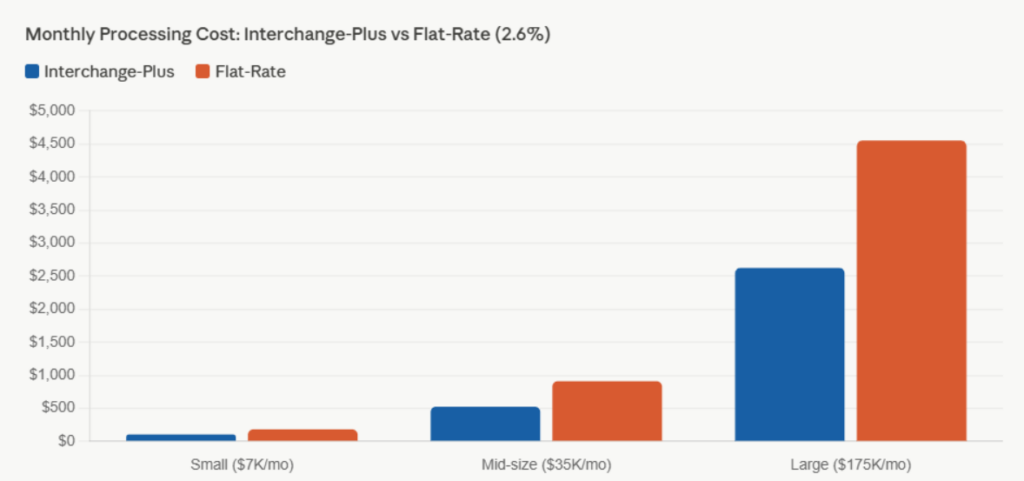

The Real Cost Difference: A Numbers Breakdown

To understand the practical impact, consider three business sizes processing cards with an average interchange rate of approximately 1.5% (a realistic mix of debit and mid-tier credit cards). Interchange-plus assumes a markup of 0.20% + $0.10 per transaction. Flat-rate pricing assumes 2.6% with no per-transaction fee for simplicity.

| Business Size | Monthly Volume | Interchange-Plus Cost | Flat-Rate Cost (2.6%) |

| Small Business | $7,000 | $105–$140 | $182 |

| Mid-Size Retailer | $35,000 | $525–$700 | $910 |

| Large Enterprise | $175,000 | $2,625–$3,500 | $4,550 |

At small volumes, the savings from interchange-plus are modest. At larger volumes, the gap becomes financially significant. A large enterprise could save between $1,000 and $1,900 per month — or $12,000 to $23,000 per year — simply by choosing the right pricing model. These are not theoretical numbers. They represent real savings that high-volume merchants miss out on when they accept flat-rate pricing without shopping around.

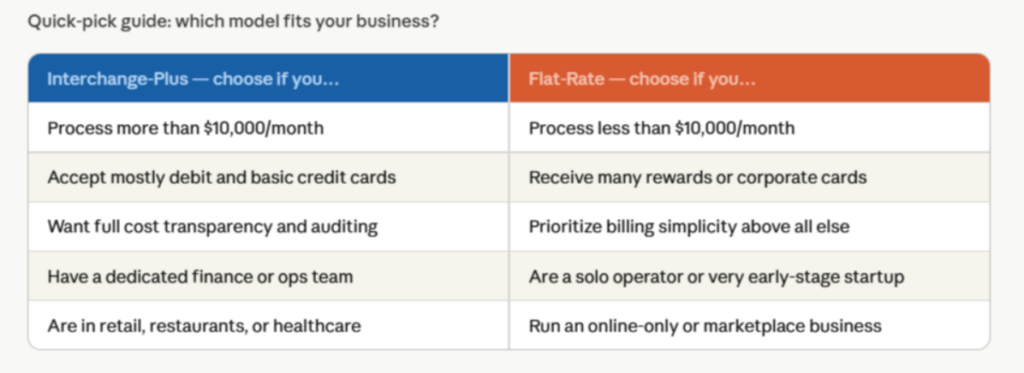

When Interchange-Plus Pricing Is the Right Choice

Interchange-plus makes the most sense when your monthly processing volume exceeds $10,000, because the savings begin to compound meaningfully at that scale. It is particularly powerful if your customer base primarily pays with standard credit or debit cards rather than high-reward or corporate cards. Businesses in retail, restaurants, healthcare, and service industries often see the greatest benefit because their card mixes skew toward lower-interchange card types.

Interchange-plus is also the smarter choice if your business values financial transparency. The detailed statements allow your accounting team to track cost trends, model future expenses, and hold your processor accountable. If you are running a larger operation or planning to scale significantly in the next 12 months, locking in interchange-plus now avoids the pain of switching mid-growth.

For a deeper look at interchange rate tables and how card networks set them, the Visa Interchange Rate Guide is one of the most comprehensive public resources available. You can access it directly from Visa’s official merchant support portal.

When Flat-Rate Pricing Is the Right Choice

Flat-rate pricing is a good fit for businesses that are early-stage, low-volume, or simply want zero administrative overhead. If you are processing less than $10,000 per month, the dollar savings from interchange-plus may not justify the learning curve or the time spent analyzing statements. A solo contractor, a part-time reseller, or a small artisan market vendor benefits far more from the instant setup and predictable billing that flat-rate processors offer.

Flat-rate pricing also makes sense when your card mix skews heavily toward premium rewards cards. Because the flat rate is fixed, it actually becomes competitive when your interchange costs would have been high anyway. A business that accepts mostly high-end corporate purchasing cards may find that flat-rate pricing costs no more — or even slightly less — than interchange-plus in practice.

Finally, flat-rate pricing is worth considering when your cash flow forecasting depends on billing precision. Knowing your exact per-transaction cost allows for tighter budgeting and simpler financial modeling, especially in early-stage businesses where every line item matters.

Beware of Tiered Pricing: The Third Option Nobody Recommends

There is a third pricing model that sits between interchange-plus and flat-rate, and it is the one most experts warn merchants against: tiered pricing. In this model, processors bundle interchange categories into tiers — typically labeled ‘qualified,’ ‘mid-qualified,’ and ‘non-qualified’ — and charge a different rate for each tier. The problem is that processors have full discretion over which transactions fall into which tier. A card that should qualify for a lower rate can be quietly downgraded to a higher tier without your knowledge. Tiered pricing obscures the true cost of processing and makes it nearly impossible to compare processors fairly. If your current processor uses tiered pricing, that alone is a good reason to renegotiate.

The Nilson Report, the payment industry’s most respected research publication, consistently shows that merchants on tiered pricing structures pay meaningfully more than those on interchange-plus when normalized for volume and card type.

How to Evaluate Your Current Pricing and Make the Switch

Start by pulling your last three months of processing statements. Look for the word ‘interchange’ on the statement. If you see a single blended rate or tiered categories, you are on flat-rate or tiered pricing. If you see line-by-line interchange categories with a consistent markup on top, you are already on interchange-plus.

Next, calculate your effective rate by dividing total processing fees by total processing volume. If your effective rate is above 2.0% and your monthly volume is above $10,000, you are almost certainly paying more than necessary. Request an interchange-plus quote from at least three processors — Helcim, Payment Depot, and Stax are all strong options with transparent pricing — and compare the markup percentage and per-transaction fee rather than the headline rate.

Check your existing contract for early termination fees before switching. Many processors impose penalties of $200 to $500 for early cancellation. Factor this into your decision but do not let a one-time fee prevent you from saving thousands annually. For additional guidance on evaluating merchant service agreements, the Consumer Financial Protection Bureau (CFPB) maintains helpful resources on payment processing disclosures.

CFPB: Understanding Payment Processing Fees — Official U.S. government guidance on financial services and merchant agreements.

Industry Context: Which Model Is Growing?

The payment processing industry is moving, however slowly, toward greater transparency. Interchange-plus pricing was once available only to large enterprise merchants. Today, processors like Helcim offer interchange-plus to businesses of all sizes, sometimes with no monthly fees at very low volumes. Stripe’s expansion of interchange-plus options through its Connect platform reflects the same trend. As small and mid-size businesses become more financially sophisticated, flat-rate pricing is increasingly positioned as a convenience premium rather than the default best choice. Merchants who take the time to compare models almost always find that interchange-plus saves money at a meaningful scale.

Conclusion: Make Your Pricing Model Work for You

There is no universal answer to whether interchange-plus or flat-rate pricing is better. The right choice depends on your volume, card mix, operational capacity, and how much you value transparency over simplicity. For most businesses processing more than $10,000 per month, interchange-plus pricing is objectively cheaper, and the numbers bear this out consistently. For early-stage businesses or those that value frictionless billing above all else, flat-rate pricing remains a legitimate and practical choice.

What matters most is that you make an informed decision. Too many merchants accept the pricing model their first processor offered without ever questioning it. Understanding the structure of your payment costs is one of the highest-return financial exercises you can do for your business. Whether you switch models, negotiate your markup, or simply confirm you are already on the best option, the knowledge pays for itself.

Frequently Asked Questions

What is interchange-plus pricing?

It is a payment processing model where you pay the actual interchange rate set by card networks like Visa and Mastercard, plus a fixed markup added by your processor. The markup is disclosed upfront and stays consistent.

Is flat-rate pricing ever better than interchange-plus?

Yes. For businesses processing under $10,000 per month or those with highly variable card mixes — especially businesses that accept many high-reward or corporate cards — flat-rate pricing offers simplicity and cost predictability that can outweigh its higher average rate.

Which payment processors offer interchange-plus pricing?

Stripe, Payment Depot, Helcim, and Stax (formerly Fattmerchant) all offer interchange-plus models. Stripe is unique in offering both flat-rate (its default) and interchange-plus (via Stripe Connect for platforms).

Can I switch from flat-rate to interchange-plus pricing later?

Yes. Most merchant service providers allow you to renegotiate your pricing model. Review your contract for any early termination fees, then request interchange-plus pricing from your current processor — or switch to one that offers it.